Digging into the GDP Data

How is the U.S Economy Doing?

Yesterday, the Bureau of Economic Analysis (BEA) released its revised estimate for Q2 GDP. Here’s what stood out and why it matters.

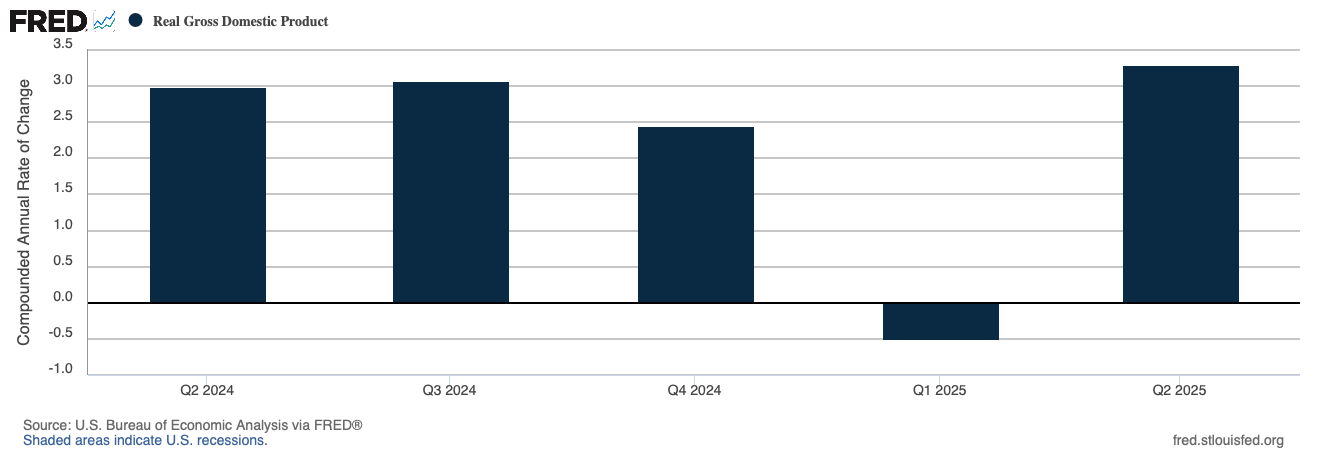

The Headline Number

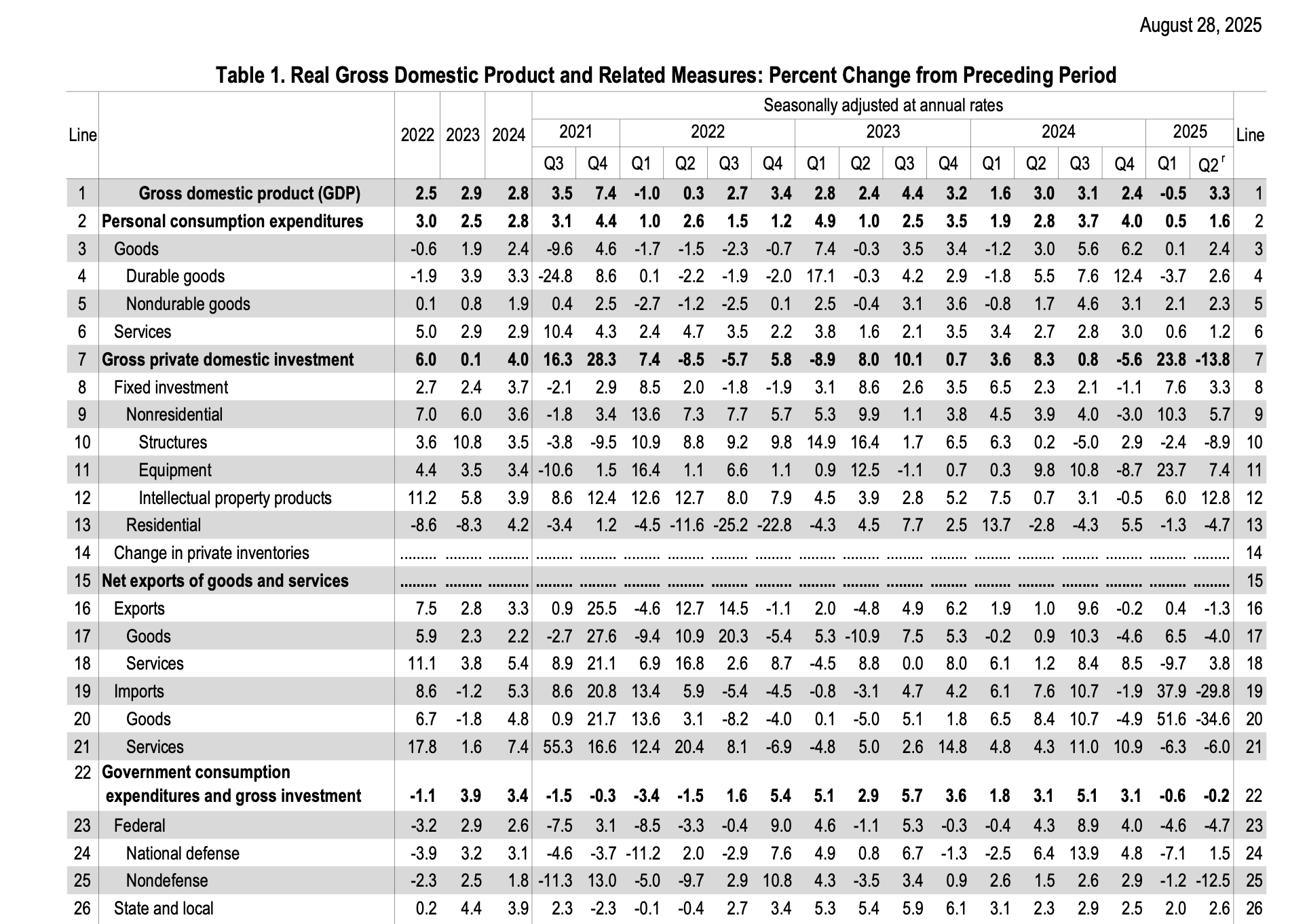

The economy grew at a 3.3% annualized pace from April to June—above the initial 3.0% estimate and the 3.1% Dow Jones forecast. The revision primarily resulted from stronger consumer spending, which increased 1.6% instead of the previously reported 1.4%. But there is more…

The Good

Households Have Cushion: Real disposable personal income jumped 5.3%, giving consumers more spending power.

Growth Beat Expectations: The economy continues to deliver upside surprises despite a challenging policy uncertainty.

The Bad

Investment Slump: Gross private domestic investment fell 11.0%, led by sharp drops in residential (–43.7%) and equipment (–20.1%) investment.

Services Weakness: Consumer spending on services—a major driver of the economy—plunged 13.8%.

Government Pullback: Federal non-defense spending declined by 12.5%, while state and local spending remained flat, providing little fiscal support.

The In-Between

Trade Boost, But Misleading: Imports collapsed 29.8% after companies stockpiled ahead of Trump’s April 2 “liberation day” announcement. Exports slipped 1.3%. While this swing added nearly 5 percentage points to GDP, it signals a decline in trade activity rather than genuine economic strength.

The Bottom Line

The headline number suggests resilience, but much of the gain is due to temporary trade effects. Import weakness inflated GDP mechanically, masking soft spots in investment, services consumption, and government spending. The underlying picture points to fragile growth ahead.

Why It Matters for You

Households: Rising disposable income provides some breathing room, but weak demand for services suggests families are tightening their discretionary spending.

Businesses: Investment cuts signal caution—firms are pulling back on equipment and construction, which could slow future productivity.

Investors: The GDP “beat” looks less durable once trade effects are stripped out, making markets more sensitive to upcoming Fed decisions and consumer data.

How’s your economy doing? Drop your answer in the comments—We would love to hear your perspective. Good, bad, or in-between?

How can there more disposable income if household debt skyrocketed? That means there was in fact *less* disposable income.