From Income Tax to Sales Tax: What Kentucky Is Really Changing

Revisiting the tax discussion

We appreciate our readers who ask questions and challenge us to go deeper. Today’s post was shaped by one reader’s question and another’s encouragement to discuss more about Kentucky’s tax policies from earlier this week. Thank you for your engagement — it helps make the conversation better.

Kentucky missed its income tax trigger by $7.5 million this year.

That narrow miss means the state’s income tax rate will not fall from 3.5% to 3% in 2027 under the current formula. But the bigger story is not about $7.5 million. It is about Kentucky’s long-term strategy to eliminate the individual income tax and rely more heavily on sales and consumption taxes.

That is a fundamental shift in how government is funded; it deserves a clear explanation, and you need to understand it.

The Plan: Gradually Eliminate the Income Tax

In 2022, the Kentucky General Assembly created a mechanism to reduce the state’s flat individual income tax rate in half-percentage-point increments, with the long-term goal of elimination.

The trigger requires two conditions:

The Budget Reserve Trust Fund must equal at least 10% of General Fund revenue.

Revenues must exceed spending, even if the income tax rate had been one percentage point lower.

If those benchmarks are met, the rate drops.

Kentucky has already reduced its income tax from 5% to 4%, and then to 3.5%. The next step would be 3%, with eventual elimination if the triggers continue to be met.

Supporters argue this makes Kentucky more competitive and attractive to businesses and higher-income earners, pointing to states like Tennessee and Florida that operate without broad income taxes.

Critics counter that eliminating the income tax does not eliminate the need for revenue — it changes where the revenue comes from and who ultimately pays.

What Replaces the Income Tax?

If income tax revenue declines, the state still must fund schools, Medicaid, infrastructure, and public safety. The most likely replacement is greater reliance on sales and consumption taxes.

In recent years, Kentucky has already broadened its sales tax base to include more services, such as landscaping, pet grooming, and certain digital products. Expanding the tax base, the amount of economic activity subject to tax, is a common way to maintain revenue when tax rates fall elsewhere.

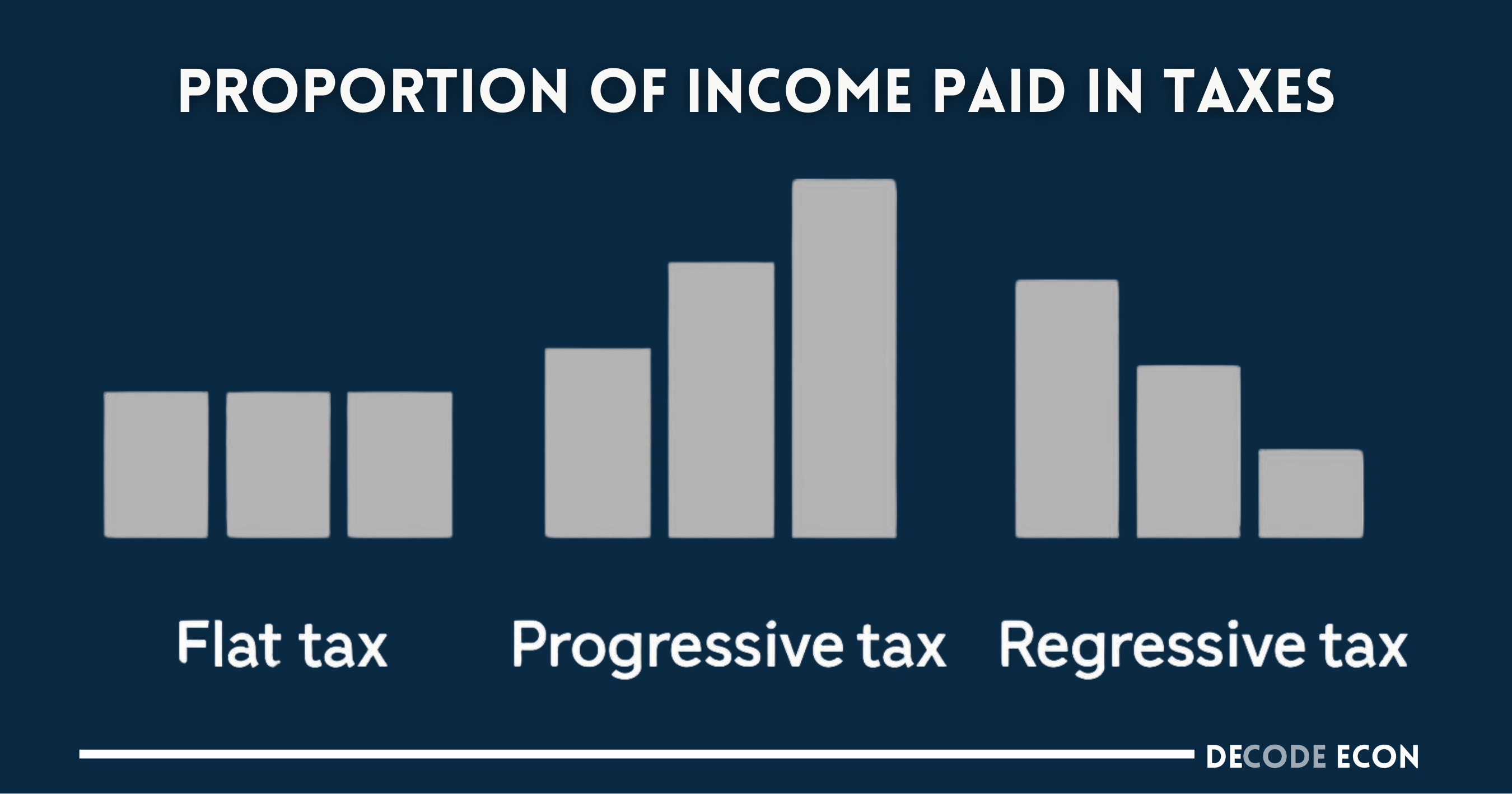

Flat, Progressive, and Regressive Taxes

This is where the economic structure matters.

A flat income tax means everyone pays the same percentage of income.

A progressive tax means that higher earners pay a larger percentage of their income as income rises. The federal income tax follows this model.

A regressive tax takes a larger share of income from lower-income households than from higher-income households.

Sales taxes are generally considered regressive because lower-income households spend a larger share of their income on consumption, while higher-income households save and invest more. Since sales taxes apply to spending, not saving, the effective burden falls more heavily, as a percentage of income, on lower earners.

That does not make sales taxes inherently bad. They are easier to administer, harder to avoid, and they capture revenue from visitors and commuters. But they do shift who bears the burden.

The Federal Context

The federal tax system is progressive: marginal tax rates rise as income increases.

Kentucky’s flat income tax is already less progressive than the federal system. Moving away from income taxes and toward consumption taxes would shift the state further toward a regressive structure relative to federal taxation.

For higher-income households, that shift may reduce the total tax burden. For lower- and middle-income households, more of the burden may move toward everyday consumption. So even if higher-income households pay more in total dollars, they may pay a smaller share of their income in taxes, while lower- and middle-income households often feel a larger impact because more of their income goes toward everyday purchases. In other words, higher-income households may still contribute more in absolute terms, but the effective tax rate as a percentage of income can decline as taxation shifts toward consumption.

This distinction is critical because it helps explain why replacing income taxes with sales taxes changes not just how much revenue the state collects, but who ultimately bears the economic burden of financing government.

That is not a moral or political claim; it is a structural one.

The Economic Tradeoff

Proponents argue that lower income taxes improve incentives to work, invest, and relocate, drawing on supply-side principles that lower marginal tax rates increase economic activity.

Opponents argue that greater reliance on sales taxes can place more pressure on lower-income households and create revenue volatility during downturns, when consumption slows.

Income taxes fluctuate with wages and profits. Sales taxes fluctuate with spending. Each comes with different risks.

The core policy question is not whether taxes should exist. It is how the burden is distributed and how stable the revenue system will be over time.

Kentucky is not simply adjusting tax rates. It is rebalancing its tax philosophy.

The Bottom Line

Kentucky is moving from a flat income tax system toward a more consumption-based model. That shift changes incentives, redistributes tax burdens across income groups, and alters the stability of state revenue during economic cycles.

You can support or oppose that direction. But understanding the structure matters.

Tax policy is not just about rates. It is about who pays — and why.

Kentucky has a 5% Capital Gains rate, Florida has none.

Kentucky has a State level property tax, Florida none.

Kentucky has an Occupational Tax, Florida none.

Vehicle Property Tax, that's Kentucky...

It's the totality of an individual's tax liablities that we should be measuring.

This is a fun conversation about wealth inequity to which I offer my own numbers according to my 2024 tax forms. Percentages represent portion of my overall pay.

Federal Withholding $181,591.02 (36.25%)

State Withholding - Maryland $28,664.35 (5.72%)

Local - Anne Arundel County $16,024.80 (3.2%)

Social Security $10,918.20 (2.18%)

Medicare $9,973.50 (1.99%)

Federal Marginal Rate - 37%

State Marginal Rate - 5.75%

Throw in another $13,000 on property tax, $300 to register my car.

Admittedly I drink 3 beers a year and don't smoke, so Pigovian Taxes don't come into play.

No Mortgage, lived in same house for a rather long time.

In the end, I pay roughly 52% of my takehome in taxes/fees. Haven't contributed to health care yet, any insurance for home or car or a single dollar towards retirement. (some of those services have their own taxable events.)

The reason I posted this was to offer an example of how higher earners not only have higher tax exposure, but the raw data that sometimes gets hidden behind class/income discussions. My overall consumption of goods isn't out of norm for a household of 2. Out to eat once a week, nothing crazy unless it's my Anniversary.

The challenge for others becomes creating a cogent argument for why my liabilities should increase. Note I didn't say decrease. While I believe there are programs that should be removed at both Federal and State levels or significantly reduced, I accept my tax burden.

Excellent explanation!! The part that is underemphasized is that when times are bad and consumption dips, the areas that suffer significantly are critical (public safety and education) - and those impacts last for years. (I lived in Tennessee for a while and would not choose to go back to a state that does not have an income tax)