The Commodification of Everything

Barnes & Noble and Foot Locker figured out where it ends. Here's what the market is telling us.

Walk into a Barnes & Noble today, and something feels off, but in a good way. The shelves aren’t organized like a warehouse. Staff may have left handwritten notes next to the books they love. There’s a local author section in the front. The store looks like it was curated by someone local who actually read the books, not by a corporate design team three time zones away.

This should not be happening. For two decades, the story of Barnes & Noble was a slow, painful decline, the kind economists use to illustrate what happens when a market shifts and a company can’t adapt. At its peak in the late 1990s, Barnes & Noble had more than 1,000 locations. By 2019, that number had fallen to 627. Borders, its main competitor, had already shut down entirely. Corporate mega bookstores had lost the fight against Amazon. We all moved to digital books and bookstores, and physical bookstores were over. The market had shifted, and the data told us that people chose convenience over tradition.

Turns out, the data was wrong.

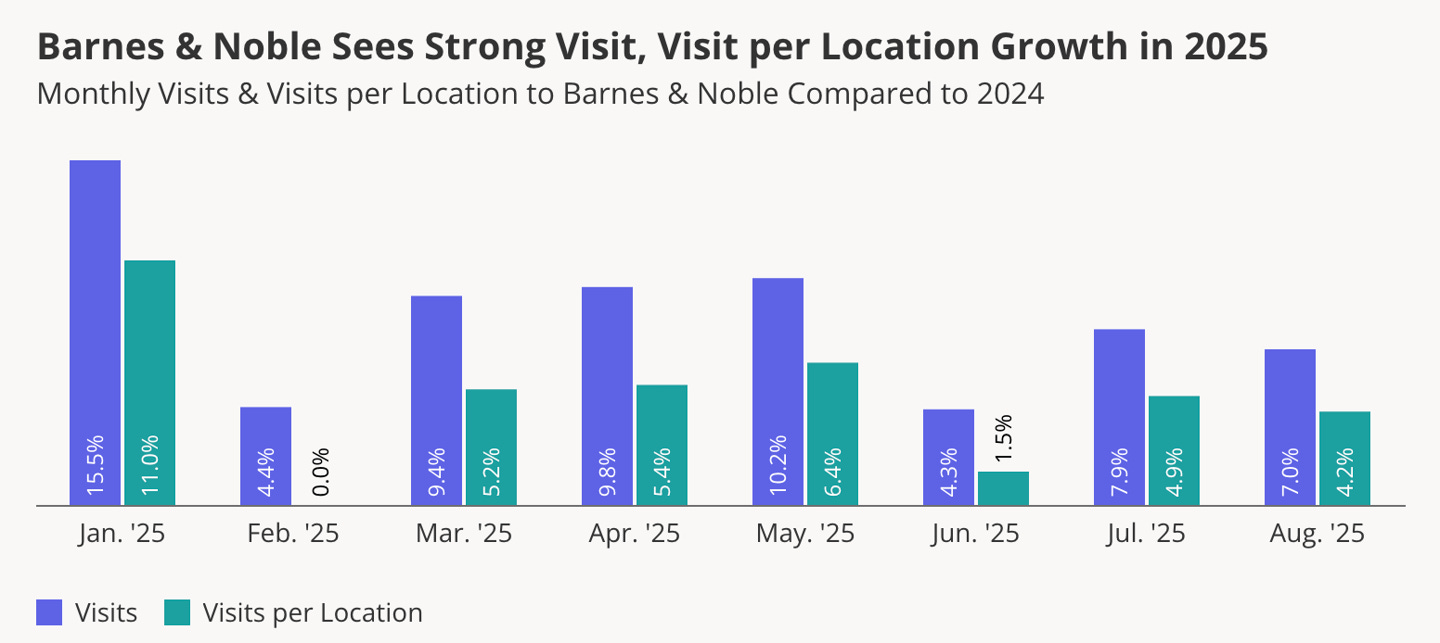

Barnes & Noble opened over 60 new stores in 2025. It plans to open at least 60 more in 2026. It aims to reach 1,000 locations, and it is growing fast enough that the number seems realistic. The company has noticed that the number and duration of visits have increased. B&N is taking notice of a market change and is leaning into it.

And it is not alone. Dick’s Sporting Goods just acquired Foot Locker for $2.4 billion and is doing something similar. It is repositioning the brand away from malls and into neighborhood storefronts, the kinds of spaces left behind by abandoned Walgreens and Rite Aid locations. We are witnessing the rise of the local shoe shop.

The market chatter said physical retail was a dying format. Consumers wanted convenience, speed, and frictionless delivery. They wanted Amazon and online shopping. The companies that survived would be the ones that accepted this and learned to compete online. The ones that didn’t would disappear.

That story had one serious problem. It confused what people said they wanted with what they were actually willing to pay for.

The Commodification of Everything

When a product becomes a commodity, what becomes scarce is the experience of getting it. Over the past three decades, we have seen experiences and relationship purchases become commodified.

Amazon solved the product problem completely. You can get virtually any book, any shoe, any item delivered to your door in two days or less. They won at the logistics game. The price is usually competitive. On pure efficiency terms, Amazon wins every time.

But efficiency is not the only thing markets price. They also price scarcity. And something strange happened as Amazon made products infinitely available: genuine human experience, the feeling of being in a place, being helped by someone who knows something, stumbling onto something you didn’t know you wanted, surrounded by people who valued it as much as you do, became rare. Those experiences are things we are longing for today.

A book recommendation from a bookseller who has read the book is a different product than an algorithm recommending the same title because 47,000 other people with similar purchase histories bought it or rated it five stars digitally. One of them feels like a personal experience, and the other is a transaction. Although the algorithm might be more accurate, the personal recommendation develops a connection. I will always value your personal recommendation over the digital one.

Barnes & Noble: The Local Inversion

The turnaround at Barnes & Noble is a deliberate structural inversion of the logic that almost killed the company.

The old Barnes & Noble model was big-box retail applied to books: enormous stores, standardized layouts, centrally planned inventory, every location interchangeable. That model made sense when the competitive advantage was selection; if you wanted a large variety of books in one place, Barnes & Noble had it. It was efficient. Then Amazon offered infinite selection from your couch, and the competitive advantage disappeared overnight.

The new Barnes & Noble, under CEO James Daunt, handed control back to the stores. They would no longer compete on efficiency but focus on experience. Local managers now make decisions about layouts, selections, and events. The store in Washington, D.C.’s historic Woodward & Lothrop building does not look or feel like the store in suburban Ohio. The Manhattan store is not the Denver store, and that specificity is the product. We are seeing the rise of local personal experiences, and buying a book is one of them.

The results are measurable. Barnes & Noble fell below 600 locations as recently as 2023. It now has over 700. In 2024, it opened more new stores in a single year than it had in the entire decade from 2009 to 2019. Some of its most loyal customers visit nearly 20 times per year, a frequency that would make most retailers envious.

Dick’s and Foot Locker: The Real Estate Arbitrage

The Dick’s Sporting Goods acquisition of Foot Locker is a different mechanism, but the underlying logic is similar. We do not know how this experiment will end, as we are in the early stages, but it is an exciting one to watch unfold.

Foot Locker’s problem was location dependency. Its stores lived in malls, and malls have been losing foot traffic for years. The brand also became dangerously concentrated, roughly 60% of its purchases came from a single supplier (Nike), giving it almost no pricing leverage and enormous vulnerability to any change in that relationship.

Dick’s saw something else. Foot Locker’s small-format stores, the kind that fit in neighborhood retail spaces, give Dick’s a way to enter markets where a standard Dick’s Sporting Goods store simply wouldn’t fit. More importantly, the collapse of Walgreens and Rite Aid left behind thousands of affordable, high-traffic, neighborhood-scale retail spaces sitting vacant across the country.

The economics of a specialty neighborhood shoe shop are fundamentally different from those of a mall anchor. This is a drastic business model shift.

The Independent Bookstore Wave

Neither of these stories is happening in isolation. Independent bookstores, the category Amazon was supposed to have eliminated permanently, have grown 70% since 2020, from 1,916 locations to more than 3,200. In 2024 alone, 323 new independent bookstores opened and only 37 closed. For every bookstore that shut down, four new ones opened.

The American Booksellers Association, which once saw its membership fall from 7,000 in 1994 to fewer than 2,000 in 2019, has now grown its membership by 18% in a single year. The revival of Barnes & Noble did not cannibalize independent stores. It validated the format and expanded the cultural permission to shop locally.

The Decode in 60 Seconds

Barnes & Noble was supposed to be dead. So was Foot Locker. Instead, both are expanding because they figured out something Amazon cannot solve.

When convenience becomes a commodity, experience becomes the scarce good. The local bookstore, the neighborhood shoe shop, the professor who knows your name, that’s what the market is rewarding. They are differentiated products, and consumers are paying a premium for personalization.

The correction is already underway in retail. It is coming for every industry that confuses efficiency with value.

The full Decode and connection to higher education is below for paid subscribers. To celebrate summer school, here is a 50% discount for an annual subscription.