The Economy Is Working. Just Not for You.

Data from the Fed, Congress, and Polymarket

In today’s newsletter, we cover three items that caught our attention:

More Evidence of a K-Shaped Economy

Congress Stopped Working

Insider Trading from Within The Government

The economy is working, just not for you!

More Evidence of a K-Shaped Economy

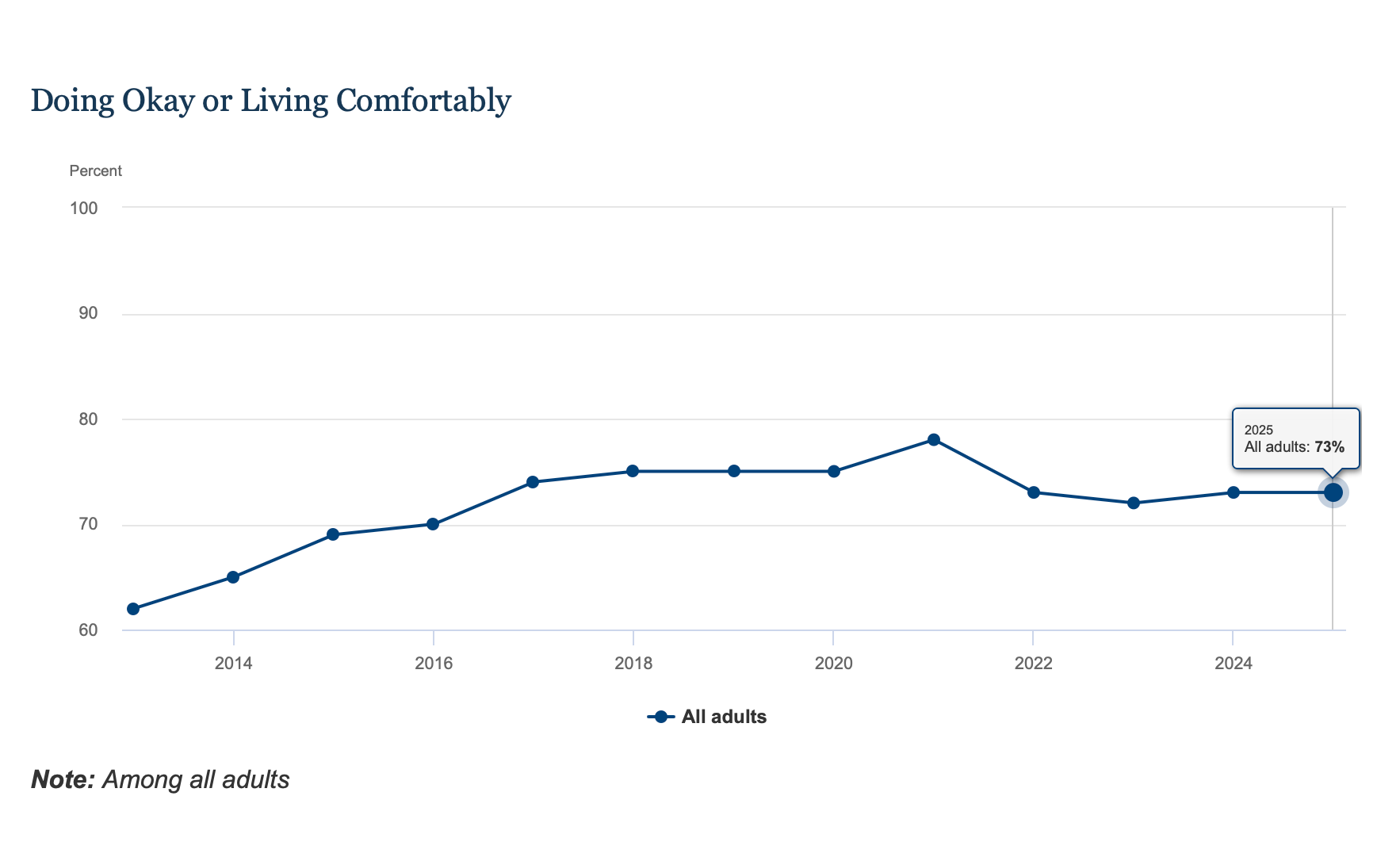

The Federal Reserve’s annual Survey of Household Economics and Decisionmaking (SHED) found that 73% of U.S. adults reported being financially stable in 2025 — a number that looks reassuring until you look at who’s pulling that average up and who’s pulling it down.

This is a K-shaped economy in action. At the aggregate level, the numbers hold steady. But beneath that surface, the split is widening. Low-income, young, and Black adults saw meaningful declines in financial well-being. Nearly 50% of adults under 30 now live with a parent, up 12 percentage points since before the pandemic. Rent delinquencies are rising. Credit card balances among people already struggling have jumped more than 35% since 2023. Meanwhile, fraud losses totaling an estimated $100 billion hit hardest among those least able to absorb them — people earning under $50,000 had a median fraud loss of $400, yet 4 in 10 of them couldn’t cover a $100 emergency from savings alone. As economist Gary Hoover of Tulane put it, things are holding steady or improving for those at the top, and declining for those at the bottom.

The fraud number is the most underreported finding in this entire report, and it's worth discussing. Most people associate financial fraud with wealthy targets: stolen investment accounts, wire transfers, and large-scale identity theft. The SHED data tells a different story. Non-credit-card fraud cost U.S. consumers an estimated $100 billion in 2025, with $56 billion borne directly by individuals.

The headline number looks fine, but it obscures a concerning story. When nearly half of young adults can’t afford to live independently, when rent delinquencies are climbing, and when the people most exposed to fraud are also the least able to recover from it, that’s not a stable economy. Gary “Hoov” Hoover is right that this isn’t sustainable. An economy where the bottom half increasingly relies on family support, credit, and deferred expenses to stay afloat is one that builds fragility into its foundation.

What It Means for You: If you’re in the lower half of the income distribution, the data confirms what you’re already feeling, and the trajectory is getting harder, not easier. If you’re doing better than average, that aggregate stability number probably feels more real to you than it does to your neighbors. This is yet another example of the economic gap in our economy. We are experiencing very different economies based on our income.

For up-and-coming researchers, this is a great dataset to work with.

Interactive Maps https://www.federalreserve.gov/consumerscommunities/sheddataviz.htm

The Survey

Congress Stopped Showing Up, and The Data Proves It

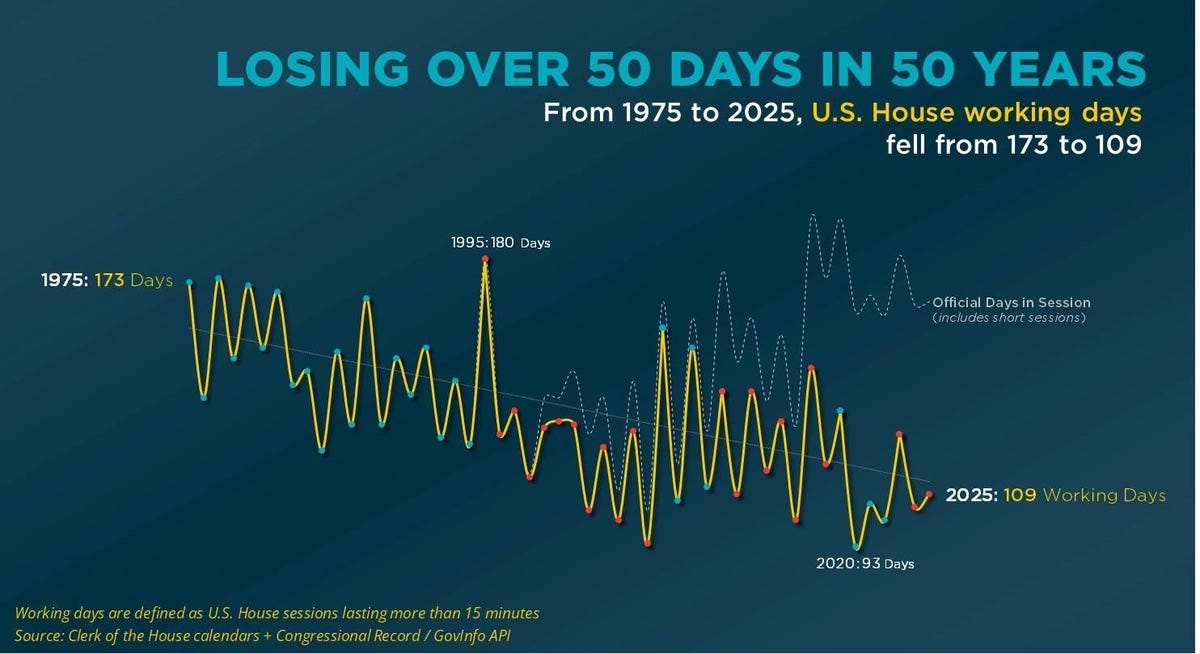

H/T to Jose Fernandez for sharing two graphs with us over the past week that highlight how little Congress is doing these days.

Here is What Happened

The current Congress is on pace to pass fewer laws than any Congress in modern history. So far, they have passed 75, compared to 700+ during peak legislative sessions in the Carter era. A second chart tells you part of why: the U.S. House worked 173 days in 1975 and just 109 days in 2025, a drop of more than 50 working days over 50 years.

The Economic Mechanism: We aren’t getting political here, but this is a story about an institutional productivity problem with real economic consequences. Congress is the body responsible for authorizing spending, setting tax policy, regulating markets, and responding to economic shocks. When it works less and passes less, the outcome is reliance on the executive branch and regulatory uncertainty, neither of which gives businesses or households the stable policy environment they need to plan. Fewer working days means fewer committee hearings, fewer markups, fewer floor votes. The pipeline for economic legislation slows down.

What People Missed: The working days chart complicates the easy narrative. It’s tempting to blame gridlock purely on polarization and chalk it up to two parties that can’t agree on anything. But you can’t negotiate what you never show up to debate. The House worked 180 days in 1995, a period of genuine partisan conflict between a Republican Congress and a Democratic president, and still managed to produce legislation. The current Congress is working 40% fewer days than the peak and producing a fraction of the output. At some point, reduced legislative output stops being a symptom of disagreement and starts being a choice.

Dr. A’s Take: There is an economic cost to legislative paralysis that rarely gets priced in. When Congress doesn’t act, uncertainty fills the vacuum, and you will often hear me say that uncertainty is expensive. When uncertainty increases, businesses defer investment. Households can’t plan around a tax policy that might change by executive order tomorrow. Infrastructure, workforce development, and safety-net programs that require reauthorization quietly deteriorate. The 119th Congress isn’t just historically unproductive. It’s unproductive at a moment when the policy agenda, tariffs, AI regulation, labor market transitions, housing, and prediction/financial markets are unusually consequential. That mismatch should concern anyone watching the economy.

What It Means for You If you’ve felt like Washington isn’t responding to the economic pressures you’re facing, the data backs you up. It’s not just that Congress can’t agree; it’s that Congress is structurally doing less work than it used to, on fewer days, producing fewer laws.

The government you chose is doing less to support you.

More Evidence the Government is Insider Trading

I was interviewed a couple of months ago by a media company that was building its economic stories. They asked me about the economic issues worth digging into and deserve to be heard. At the top of my list were the unregulated prediction markets and the rampant insider trading on these platforms.

In a recent CBS article and a 60 Minutes episode, they reported on a data analytics firm, Bubble Maps, that identified nine anonymous Polymarket accounts that placed bets on U.S. military action against Iran. These bets covered detailed events like the timing of strikes, the removal of Iran’s supreme leader, and a ceasefire announcement, and won 98% of them across more than 80 wagers.

The payout netted over $2.4 million. Separately, $800 million was wagered on oil prices dropping roughly 15 minutes before President Trump publicly posted about progress on a ceasefire with Iran. Federal investigators are now probing the oil trades. Also, an Army master sergeant was indicted last month for allegedly using classified information to bet on a special operations mission, netting over $400,000.

The Economic Mechanism

Prediction markets are supposed to work by aggregating information. Thousands of bettors each contribute a small piece of what they know, producing a price that reflects collective probability. The theory is beautiful; better information improves market outcomes. We are all supposed to win!

But what happens when one party in a transaction has information that others don’t? It increases the likelihood that insiders will trade on nonpublic information. This isn’t market improvement; it is insider trading. In regulated financial markets, insider trading is illegal.

The Polymarket case adds a twist: because every trade is publicly visible on the blockchain, the position is transparent but anonymous in real time. What that means is detection is possible, but prevention is nearly impossible without identity verification. The platform has resisted making the identity of position holders public. There’s also a national security threat here that standard insider trading analysis misses: if these bet positions on war events are public, American military movements eventually become readable in market data before they become public. If Bubble Maps could do it, adversaries can as well.

Dr. A’s Take: Prediction markets are being sold as the next frontier of financial participation, a way for ordinary people to put real money behind what they believe about the world. For those of us working in financial literacy and behavior, we are seeing an increase in young adults and kids participating in prediction markets. The “betting and gambling” wave is impacting the financial futures of the next generation of Americans. Your kids are impacted, and it is worrisome.

In this example, what worries me beyond the individual losses is what this does to institutional trust over time. The moment people realize that someone in a government situation room is using confidential information to make money, they will lose trust in both prediction markets and their government.

Prediction markets are behaving like financial markets and require the same regulation and insider-trading protections.

Here is a 60 Minutes Reel that sparked this take.

The K shaped economy and prediction markets have spurred a lot of discussion. The unproductive congress is certainly something I am aware of, but I had not really considered the implications. What a great insight! I suppose future congresses will inherit a house with significant "deferred maintenance!"

Nice piece, but I am afraid I have a few critiques:

I'm skeptical that a declining number of bills reflects less legislative work. The story would be more compelling if the data was more granular (showing page or word counts). Here is a quote from govhttp://track.us:

"Congress has typically enacted 4-6 million words of new law in each two-year Congress. However, those words have been enacted in fewer but larger bills. Therefore, the generally decreasing number of bills enacted into law does not reflect less legislative work is occurring."

https://www.govtrack.us/congress/bills/statistics

Over time, politicians have learned they can get more politicians on board by wrapping legislation into big omnibus bills. That way, everyone will vote on it for the pieces they like, despite the presence of elements they dislike.

As for prediction markets, the whole idea is to aggregate information that is not publicly available or easily accessible. That may have undesirable effects in some instances (insider trading) which could lead to loss of faith in government if violations go unpunished, but it is a non sequitur to say that this would lead to a loss of faith in prediction markets. If anything, it makes prediction markets much more reliable. (You may have meant that it makes individuals with little new information less inclined to participate in prediction markets, and that is exactly the outcome we should desire if we want the prediction to be accurate.)