Your Retirement, Oman's Geography, and the End of an Era

In this edition

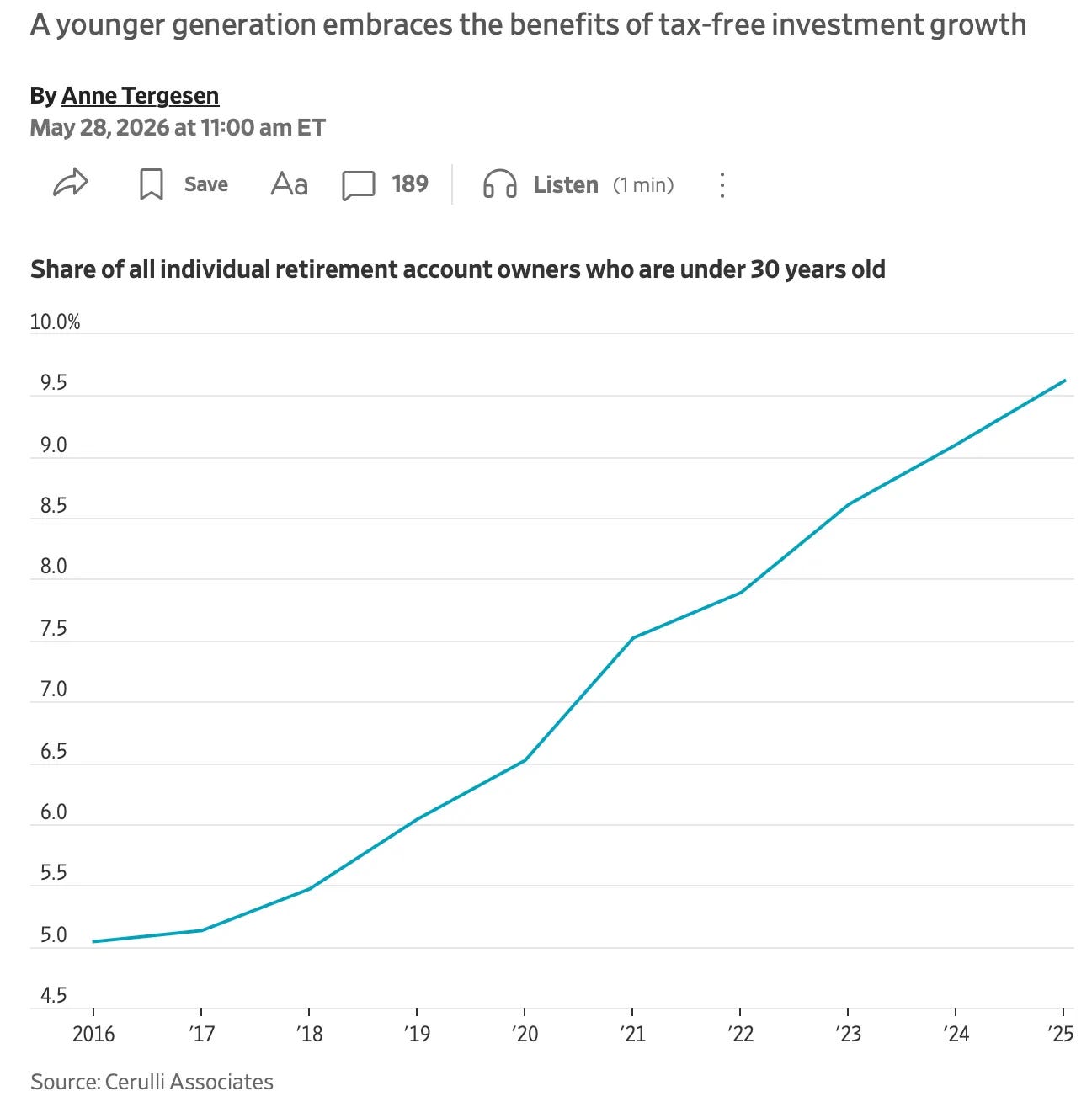

Why Gen Z may be winning the retirement math

What my home country of Oman is betting its future on

What Alan Greenspan's death at 100 tells us about the cost of being wrong at the right moment.

Gen Z Is Betting on the Future — And the Math Might Be Right

What Happened

Gen Z now accounts for 34% of IRA contributions so far this year, according to Fidelity data, and the share of IRA owners under 30 has nearly doubled since 2016. These aren’t trust fund kids parking windfalls; this is a generation that watched their parents navigate the 2008 crash, deciding early that waiting isn’t a strategy.

This is a shift, and it is worth discussing. More on this in Friday's post to our paid subscribers.

The Economics of Roth IRAs

A Roth IRA is a tax-timing trade: you pay taxes on contributions now in exchange for tax-free growth later. The bet is that your future tax rate will be higher than your current one, which usually pays off most for young, lower-income earners who are almost certainly near the bottom of their lifetime earnings curve.

The opportunity cost is real (that money can’t be easily accessed before retirement without penalties), but compound growth over a 40-year horizon makes early contributions disproportionately valuable.

If you are looking to invest in a Roth IRA, here is what you need to know for 2026:

The contribution limit is $7,500 if you are under 50, and $8,600 if you are 50 or older. The extra $1,100 is a catch-up contribution designed for people who started late. You can make the full contribution if your Modified Adjusted Gross Income is under $153,000 (single) or $242,000 (married filing jointly). Above those thresholds, your contribution limit phases out and disappears entirely at $168,000 (single) or $252,000 (joint).

Watch out for this:

It turns out that a common mistake is opening an IRA account and funding it but never investing the funds. The funds must be invested; otherwise, you are just parking your cash in an IRA account.

Oman Quietly Builds a Second Economy

What Happened

Oman closed 2025 with a budget deficit of roughly $1.2 billion. That is 26% lower than projected, thanks to oil prices running above the $60/barrel assumption the budget was built on. More interesting than the deficit number: the transport and storage sector contributed $2.3 billion to GDP, and the government has set a formal target for logistics to become the country’s second-largest economic sector by 2040.

The Economics of Strategic Development

This is economic diversification as deliberate industrial policy. Oman is using geographic advantage (Oman sits at the mouth of the Persian Gulf, outside the Strait of Hormuz) to build infrastructure that generates revenue independent of oil prices. Port investment and free trade zones create agglomeration effects: once the infrastructure exists, the activity clusters around it. The goal isn’t to move containers; it’s to make Oman a structural node in global supply chains so that when oil revenue falls, something else holds the economy up.

A note from Dr. A

I miss Oman. Growing up there, I watched a country develop, and its policies shaped it into one of the most stable economies in the Gulf. The growth of the 80-2000 was built almost entirely on oil revenue and careful fiscal management. The question my generation of Omanis grew up with was always the same one: what happens when the oil runs out? What I’m watching now is my home country making the most important economic bet of my lifetime: that geography and infrastructure can replace a resource that won’t last forever. I don’t know if it will work. But I know the economics behind why they’re trying.

In 2020, I presented on this topic at Majlis Al Khonji in Oman. My advice was to lean into Oman’s geographic comparative advantage. I am glad to see those investments paying off.

Alan Greenspan, 1926–2026

What Happened

Alan Greenspan, who served as Federal Reserve Chair from 1987 to 2006, died Sunday at 100. His tenure was the second-longest in Fed history, second to William McChesney Martin. His leadership of the Fed spanned some of the most consequential moments in modern economic life. He presided over the long expansion of the 1990s, responded to crises in real time, and left office three years before a financial crisis that critics argue his regulatory philosophy helped create.

Five moments that defined his tenure:

Black Monday (1987) — In his second month on the job, the Dow dropped more than 22% in a single day. Greenspan moved immediately to inject liquidity into the financial system. It worked. That response established the template for every Fed crisis intervention that followed.

The “irrational exuberance” speech (1996) — Greenspan warned publicly that asset prices might be dangerously disconnected from fundamentals. Markets barely blinked. The dot-com bubble kept inflating for four more years, and then it didn’t.

The dot-com crash (2000–2001) — When the bubble burst, Greenspan cut rates aggressively. The recession was short. The lesson policymakers walked away with was that the Fed could manage the downside of any asset bubble. That would come back to haunt them later on.

Post-9/11 rate cuts (2001) — Rates fell to historic lows following the attacks. Combined with financial deregulation, cheap money flowed into housing. The seeds of the next crisis were planted here, though few saw it at the time.

The 2008 reckoning — Greenspan testified before Congress in October 2008 and admitted he had found a “flaw” in his ideology — the belief that financial institutions would self-regulate in their own self-interest. It was a rare public acknowledgment from a central banker that a worldview, not just a policy, had failed.

The Economic Mechanism

The “Greenspan put” — the expectation that the Fed would intervene to support markets during downturns — became one of the most consequential implicit policies in modern financial history. When market participants believe a safety net exists, they price risk differently. They take more of it. Whether that moral hazard contributed to the leverage that made 2008 so destructive is still debated, but the mechanism is clear: expectations about central bank behavior change everyone's behavior. Greenspan personified the argument that central bank credibility is itself a policy tool — and the corollary that it can cut both ways.

I keep coming back to Greenspan’s phrase: irrational exuberance. He said it in 1996, four years before the dot-com bubble burst. He saw something, mentioned it but never did anything about it.

I think we are in a similar moment. The excitement around AI has lifted markets for three years running. That is not inherently bad, but asset price inflation driven by a single technology thesis looks a lot like 1999. And the contagion risk reminds me less of the dot-com crash and more of 2008, when Wall Street’s exposure to mortgage-backed securities was supposed to remain contained to the people holding them. We learned the hard way that our financial system does not contain risk; it distributes it across the market.

Here is what concerns me most: the AI-driven market rally has deepened the K-shaped economy. The top of the wealth and income distribution is where the assets that have appreciated are held. They are also the reason this economy continues to grow. That is a fragile foundation. When the engine of growth is concentrated at the top, the correction, when it comes, does not stay there.

Greenspan found a flaw in his ideology in 2008. I hope we are not building the conditions for someone to say the same thing about ours.

I find the omani story interesting. They are developing better than other near east conter parts. I feel like the Saudi approach was throw atuff at wall for the longest time.

Fidelity's dataset uses "averages" rather than "median"...

Covid stimulus checks - most of my co-workers put that money into investment vehicles for their kids, it was free money for them. Some older Gen Z did the same on their own.

The market is ugly with overvalued stocks giving wealth effect, we see a crash, some of those amounts are going to take a hit.

My MIL is not a rich person and during her "shed some assets to avoid taxes" phase (encouraged by me), that money was put in grandkids savings. The deal was the money wasn't to be spent but invested for the future. $500 seed money has done alright... but absolutely is reflected in the overall rate/amounts.

*We also see some of that influencer money being set aside since plenty of them have no real marketable skill to sustain them in the future. 19 yr olds on OF making $200K a month for feet pics comes to mind! (We have strange priorities for what represents "work" and its payoff?)