Can Kentucky Cut Taxes and Still Compete?

Kentucky’s Budget and the Growth Question

If you are a business owner, executive, or taxpayer in Kentucky, the current budget debate should matter to you.

The House budget proposal reduces funding across higher education, K-12 schools, Medicaid, and state employee health plans while structuring the budget in a way that could trigger additional income tax cuts. According to analysis from the Kentucky Center for Economic Policy, higher education funding would fall roughly 15 percent over the biennium, K-12 funding would remain below inflation-adjusted levels from 2008, and Medicaid projections appear underfunded relative to executive estimates.

At the same time, the state’s Budget Reserve Trust Fund remains largely untouched, and overall appropriations are set below projected revenues in a way that could enable further income tax reductions.

The narrative behind this approach is familiar: lower taxes will attract businesses and residents, expand the tax base, and strengthen the economy.

That is a powerful promise. The question is whether it holds under today’s conditions.

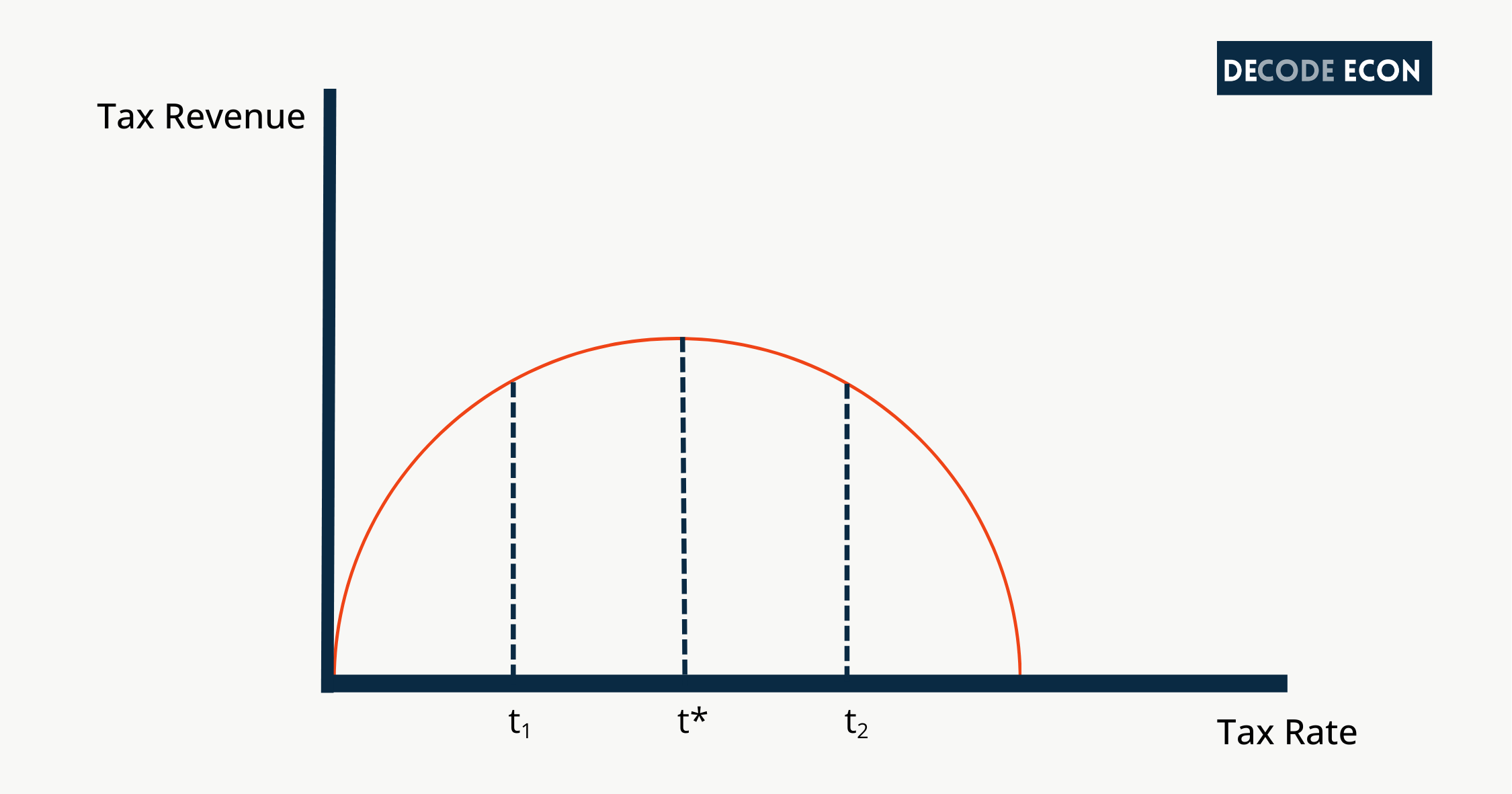

The Economics: The Laffer Curve and Interstate Competition

The intellectual foundation for many tax-cut arguments traces back to Arthur Laffer and the Laffer Curve. The idea is straightforward. At a zero percent tax rate, the government collects no revenue. At a 100% tax rate, economic activity collapses, and revenue again falls toward zero. Somewhere in between is a rate that maximizes revenue.

If a state taxes above the optimal point, cutting rates could increase economic activity enough to offset some or all of the lost revenue.

But that outcome depends on conditions that are rarely discussed in public debate.

First, the existing tax rate must actually be above the revenue-maximizing point. Second, other states must not respond by cutting their own taxes. Third, the revenue reduction should not undermine the public services on which businesses rely.

Today, many states are lowering income taxes at the same time. When everyone cuts, the competitive advantage shrinks. What remains is a smaller shared revenue base.

The Broader Pro–Tax Cut Argument

Supporters of income tax reductions do not rely solely on the Laffer Curve. Organizations like the Tax Foundation and the Cato Institute argue that lower marginal income tax rates improve a state’s competitiveness by reducing distortions to labor supply, entrepreneurship, and investment. They emphasize that simpler, flatter tax structures can attract mobile capital and high-income earners in an era when businesses and workers have more geographic flexibility than ever before.

From this perspective, income tax reductions are less about maximizing revenue and more about improving long-run economic dynamism. Lower marginal rates may encourage business formation, increase after-tax returns on investment, and send a signal that a state is open to growth.

These arguments are not trivial. Tax competition between states is real. Capital is mobile. High-skilled workers often have options.

The economic question is not whether tax policy matters. It does. The question is how much it matters relative to the public investments that sustain productivity. After all, the government still has a responsibility to provide services that we all, firms and individuals, rely on.

What a 1% Rate Cut Looks Like in Practice

To Individuals

Let’s make this tangible. Since 2023, Kentucky has reduced its flat income tax from 4.5% to 3.5%

For a worker with $60,000 in taxable income:

At 4.5% state income tax totals $2,700

At 3.5% state income tax totals $2,100

Annual savings of $600

For a worker earning $100,000 in taxable income:

At 4.5% state income tax totals $4,500

At 3.5% state income tax totals $3,500

Annual savings of $1,000

Those are meaningful savings for households. Kentucky has already reduced its flat income tax from 4.5% to 3.5% since 2023. A further 1% reduction would yield a similar arithmetic result.

Now consider the state level.

If Kentucky’s taxable income base is roughly $200 billion (total personal income in Kentucky for Q3 of 2025 is $281 billion), then a 1 percentage point reduction in the flat tax rate would reduce revenue by about:

1% of $200 billion = $2 billion

For reference, $2 billion is roughly equivalent to 12.74% of Kentucky’s $15.7 billion General Fund ending fiscal year 2025.

That is a static estimate, meaning it assumes no change in behavior.

Supporters of tax cuts argue that some of that $2 billion could be offset over time through increased economic activity, higher labor participation, or business formation.

Critics argue that even with behavioral responses, a meaningful revenue gap would remain.

The core tradeoff becomes clearer when you see the numbers. A 1% rate cut delivers hundreds of dollars per household. It also potentially removes billions from the public budget.

The policy question is whether the foregone revenue would have generated more or less long-term economic value if reinvested in education, infrastructure, healthcare, or workforce development.

The Economic Development Reality

For business leaders, this is not an abstract theory. Workforce quality, infrastructure reliability, public safety, and health systems are inputs into productivity. When those inputs weaken, long-term growth suffers. Economic development organizations are working hard to attract businesses to the area and increase economic opportunities. The decision to relocate is a function of both taxes and economic infrastructure.

Companies are attracted to areas where people can learn, work, and live. They want to relocate to areas with educated populations, strong public transportation, beautiful parks, and readily accessible healthcare.

As Ashby Drummond, Director of Research and Strategy at BE NKY, explained in our recent conversation,

Companies are often willing to operate in higher-tax jurisdictions when they perceive that those revenues are being reinvested in ways that directly support business needs and help address structural challenges.

That insight reflects a broader shift in corporate decision-making.

Taxes create distortions, yes. But public goods create positive spillovers. When the conversation focuses only on the cost of taxation without examining the return on public investment, we are evaluating only half the balance sheet.

Drummond also noted that workforce mobility has changed significantly over the past several decades. We previously discussed how workers today are less likely to relocate, which means companies increasingly position jobs in places where people already want to live. As a result, corporate location decisions are shaped not only by cost considerations but also by local amenities and public investments, particularly in education, childcare, housing, and infrastructure.

These quality-of-life factors, many of which are supported through tax revenues, now sit at the center of economic development strategy.

The Manufacturing Market

Consider advanced manufacturing, a major economic cluster in Northern Kentucky, as announced by BE NKY recently. Major investments like EV battery production, automotive expansion, aerospace and aviation, and distribution and logistics require engineers, skilled technicians, data analysts, and supply chain managers. Those workers are trained in Kentucky’s universities, community colleges, and technical programs.

If higher education funding falls by 15 percent while enrollment pressures remain high, institutions will either increase tuition, reduce program capacity, or scale back specialized programs. Over time, that constrains the local talent pipeline.

Businesses may still be attracted by tax incentives, but if they cannot hire locally at scale, the long-run cost of recruitment and relocation rises.

The Bottom Line: What This Means for You

If you are building a company or managing one, your success depends on more than your marginal tax rate. It depends on the quality of the talent pipeline, the stability of institutions, the strength of transportation networks, and the health of the labor force.

If you are a citizen, your quality of life depends on the same ecosystem.

The real policy question is not whether taxes are good or bad. It is whether the mix of taxation and public investment supports long-term competitiveness.

A state can lower taxes and still grow if it maintains strong public investments. A state can also lower taxes and slowly erode the foundations that make it attractive in the first place. In a competitive environment where multiple states pursue similar strategies, it becomes harder to satisfy those conditions.

As business leaders and engaged citizens, we should ask a more disciplined question: are we optimizing for sustainable growth, or for a short-term headline?

Capital can be attracted with incentives, but productivity must be built.

The reduction in income based taxes would need to be offset by increased economic activity. A $1 reduction would need $5 of activity (assuming 20% at Federal level, individual States obviously differ.) Corporations are sensitive to rate changes given the longer planning cycle (but that becomes an off-shoring debate?)

Laffer needs marginal rates between 55-75% to maximize revenue, good luck to any politician trying to push that through.

*The move to Florida currently is Service-based companies who are immune from manufacturing concerns, as an exmaple of portable money. But Florida is also an outlier given the size of the tax-income derived from tourism ($33B in 2024 with a $117B state budget, roughly the same as NYC.)

I'm not in a border city, but I've heard these debates about tax differences at the municipal level when trying to find a home in two neighboring cities. Homes sell like hotcakes in the high-tax city because of how great the school is, while homes in the low-tax city sell for much less and sit on the market for much longer.

I wonder how much these sorts of state-level decisions influenced Moretti's Great Divergence narrative a 10+ years ago?