What's your financial number?

Why are we rushing?

Last week, I wrote about how personal finance education without economic education is creating a generation of financially anxious people.

One of the biggest sources of that anxiety is retirement:

Will I have enough money to live on?

This anxiety is driven by several factors:

The shift from pensions to 401(k)s has placed a major responsibility on individuals, a role previously handled by employers or professionals. See video below.

There is a growing fear that Social Security is financially unstable and may not fully support future generations.

And most critically, people are told to save as much as they can, as fast as they can, in order to retire.

Item 3 is the most frustrating to me. Everyone is rushing towards a goal that they have not defined.

It’s vague. It lacks a clear target. And it creates the feeling that if you’re not aggressively saving at all times, you’re failing.

An Unidentified Target

If you are starting your career, or revisiting your financial plan, ask yourself:

Do you have a retirement goal? What is your number?

There are several ways to estimate your retirement savings goal (and yes—standard disclaimer—this is not financial advice. It is strictly educational).

A simple framework:

Calculate your annual spending.

This is why tracking spending and budgeting matters (as I’ve discussed before).Multiply that number by 25.

Why 25? This is based on the idea that you can withdraw about 4% annually in retirement (adjusted for inflation) and live comfortably.

An Example

Let’s say you spend $80,000 per year.

To maintain that lifestyle in retirement:

$80,000 × 25 = $2,000,000

That’s your number. This estimate assumes no Social Security support (see point #2 above). Your goal is to get to $2,000,000. Do not move the goal post!

Now What?

Your goal is to reach $2,000,000 by the time you retire.

How you get there is a choice.

It’s fundamentally a tradeoff between current consumption and future consumption:

You can save aggressively now, sacrificing current consumption for more freedom later.

Or you can save less, enjoy more today, and potentially work longer.

Neither is wrong. It’s a matter of preference, and this is what we do not talk about enough.

Do not let society bully you because you have different preferences.

But the way personal finance is often taught makes it seem like there is only one “correct” choice: be aggressive, or you’re failing. That’s not true.

What Actually Helps You Reach Your Goal

Time

The longer your money is invested, the more compounding works in your favor.Returns

Higher returns accelerate growth—but typically come with higher risk.Diversification

Managing risk through diversification helps reduce volatility over time.Contribution Rate

How much you consistently invest matters more than people think.Reducing Your Expenses

A lower burn rate means you need a smaller retirement number, making your goal more achievable. Do not fall for lifestyle creep, but thats a discussion for another time.

How Much to Save

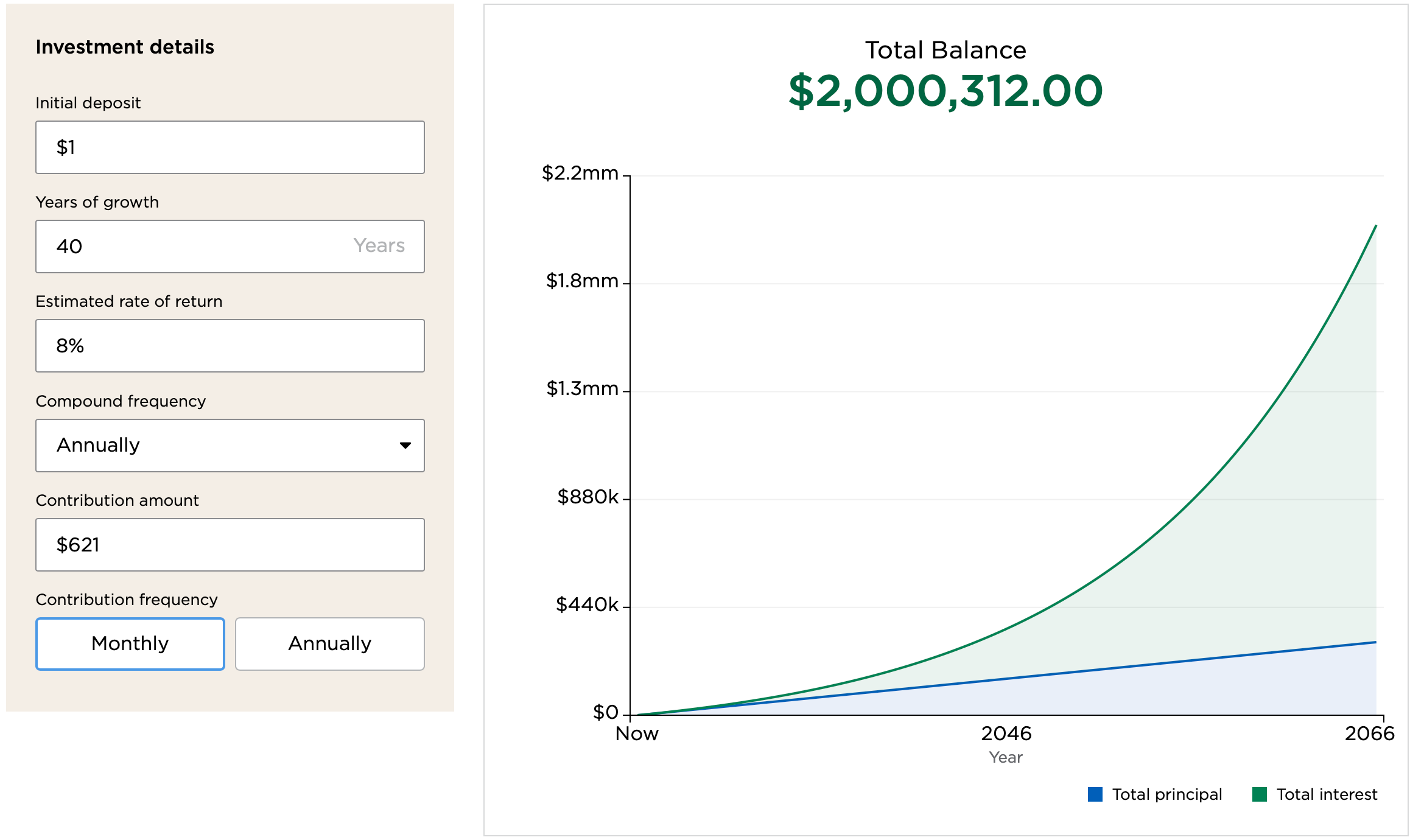

I love Nerdwallet’s compound interest calculator. In this example, I used the following information.

Here’s an example using simple assumptions:

You start with $1 saved (it doesn’t allow you to start with 0!)

You invest for 40 years (e.g., from age 22 to 62)

You earn an average return of 8% annually (based on historical averages)

Returns are compounded once per year (a conservative assumption)

Under these conditions, consistent investing over time can grow your savings to around $2 million.

The exact monthly contribution needed depends on your starting point—but the takeaway is what matters: There is a path to reaching your number. In this example is $621 monthly.

For tax considerations and proper diversification, it’s worth speaking with a professional to design the right strategy for you.

This isn’t about chasing a vague goal. It’s about understanding that, with time, consistency, and compounding, your goal is achievable.

You are probably asking yourself, where do I get $621 from? That is the next installment of this personal finance series.

Watch

Ever wonder what happened to pensions? In this video, I cover the decline of the pension system and how 401 (k) accounts became so popular. Most importantly, we discuss the pros and cons of the 401K retirement system. The shift from Defined Benefit to Defined Contribution has both advantages and disadvantages.

This reminds me that it is a long-run game. Many social platforms push this one way ideology of investing/saving, but the truth is there are so many different paths and many decisions to be made along those paths. It's content like this that helps keep me sane while on my own path.

A much needed reminder that wealth isn't built over night. I think many people forget or confuse that. It is a long game just like retirement is a long game. I blame influencer culture though.